Before I show some of those tests I thought I would point you to the rules of FTDs and some of the assumptions I used in testing them. I basically followed all of the rules as IBD laid them out. Two rules that IBD has never clearly defined are what entails “success” or “failure”. I defined “failure” to be a close below the intraday low of the bottom prior to the FTD. I defined “success” as a move either 1) twice as large as the distance from the low of the potential bottom to the close of the FTD, or 2) a new 52-week high. More detailed explanations of the rules may be found using the link below:

http://quantifiableedges.blogspot.com/2008/01/ibd-follow-through-days-pt-1-are-they.html

Whether a FTD successfully predicts a rally is not an indication of whether someone trading individual stocks using IBD’s techniques would make money or not. What it does measure is the usefulness of FTDs as a market timing indicator. I believe this is a fair way to test them since IBD claims they are valuable in identifying when downtrends are ending and new uptrends are emerging.

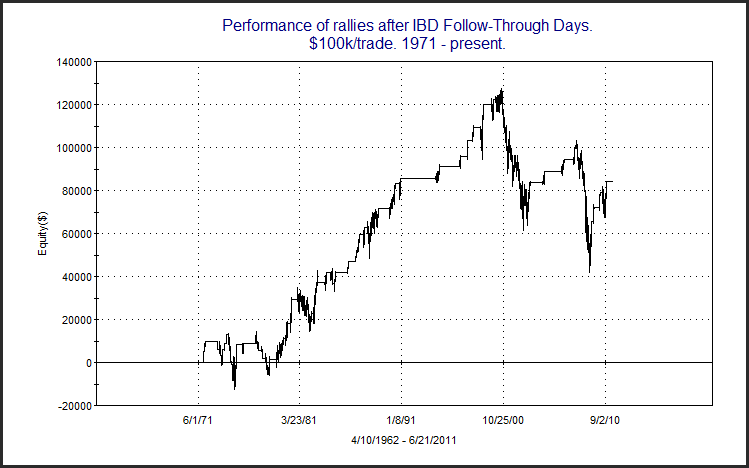

Using the original parameters as described in the post I linked to above there have been 74 FTDs since 1971. Thirty-eight of them (53%) led to successful rallies. This is an interesting stat but it doesn’t tell the whole story. Below is an equity curve that I don’t believe I’ve ever shown prior to last night's subscriber letter. It shows how someone trading the SPX would have performed using FTDs as a buy trigger and then exiting the trade when the rally either “succeeded” or “failed”.

As you can see FTDs worked very well during the long bull market of the 80s and 90s. But in the 70s, and again since 2000, FTDs have struggled as a market timing tool.

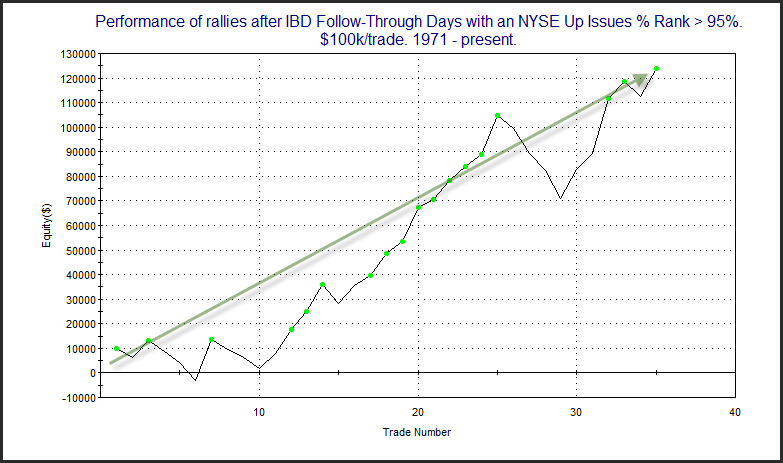

As I mentioned earlier, breadth was also very strong on Tuesday. When compared to the past year the Up Issues % on the NYSE was higher than 98.4% of all days. I used the Up Issues % Rank to normalize breadth over the long test period, and broke down FTD results based on those times the 1-yr % Rank was > 95% and those times it was < 95%. First let’s look at times like now where the NYSE Up Issues % Rank was > 95%. (An Up Issues % Rank > 95% means that a higher % of issues traded up today than in 95% of all days over the past year.)

In this case 22 of 35 FTDs (63%) have been followed by successful rallies and gains have been fairly steady over the years.

Now let’s look at FTDs that came without very strong relative breadth.

Results here were never strong and they’ve turned quite negative in recent years. Rather than a 63% success rate as happened with strong breadth, only 44% of instances here succeeded.

So for those who may not have considered it in the past, examining breadth strength on FTDs seems a worthwhile endeavor.

2 comments:

Rob,

This is great information. But wouldn't a better measure of success be from the FTD to when IBD goes to "Market in correction" for the first time. Then you are allowing for equity gained during those periods when the market is under pressure before resuming its uptrend. Another question: why doesn't your equity grow significantly after the 9/1/10 FTD?

Nat

Hi Nat,

I'm not testing IBD. I'm testing FTDs. I don't care when IBD says "market in correction". I just want to quantify how well FTDs do at predicting rallies. Also, finding out when they say "market in correction" would be a very arduous task, and lastly the criteria and people making the call might change over time.

The way the study was designed 9/1 was not considered a FTD, because there was still a FTD active from July that had neither "succeeded" nor "failed". The July FTD was deemed a success on 11/4/10 when a new 52-week high was made.

Traders who are interested in changing parameters and studying FTDs more may purchase the FTD Tradestation Study code from the website.

http://www.quantifiableedges.com/code.html

Best,

Rob

Post a Comment